Welcome to 2024! Things are looking up after a challenging investment year.

LLMs: Back in my June post, I expressed skepticism about LLM hype. I have even higher conviction now that there’s a bubble here. Angel investors jumping into secondary offerings for Open AI and Anthropic at premiums to the last priced round may be taking more of a risk than they realize. The technical moat appears to be smaller than initially thought, as the costs for training and inference drop rapidly AND researchers figure out how to optimize for particular use cases with models an order of magnitude smaller than GPT-4. On top of that, for the Open AIs of the world, there are still copyright risks, governance risks, and partnerships with Big Tech that will see those incumbents capture a significant portion of value.

Thanks for reading Contrarian Angel! Subscribe for free to receive new posts and support my work.

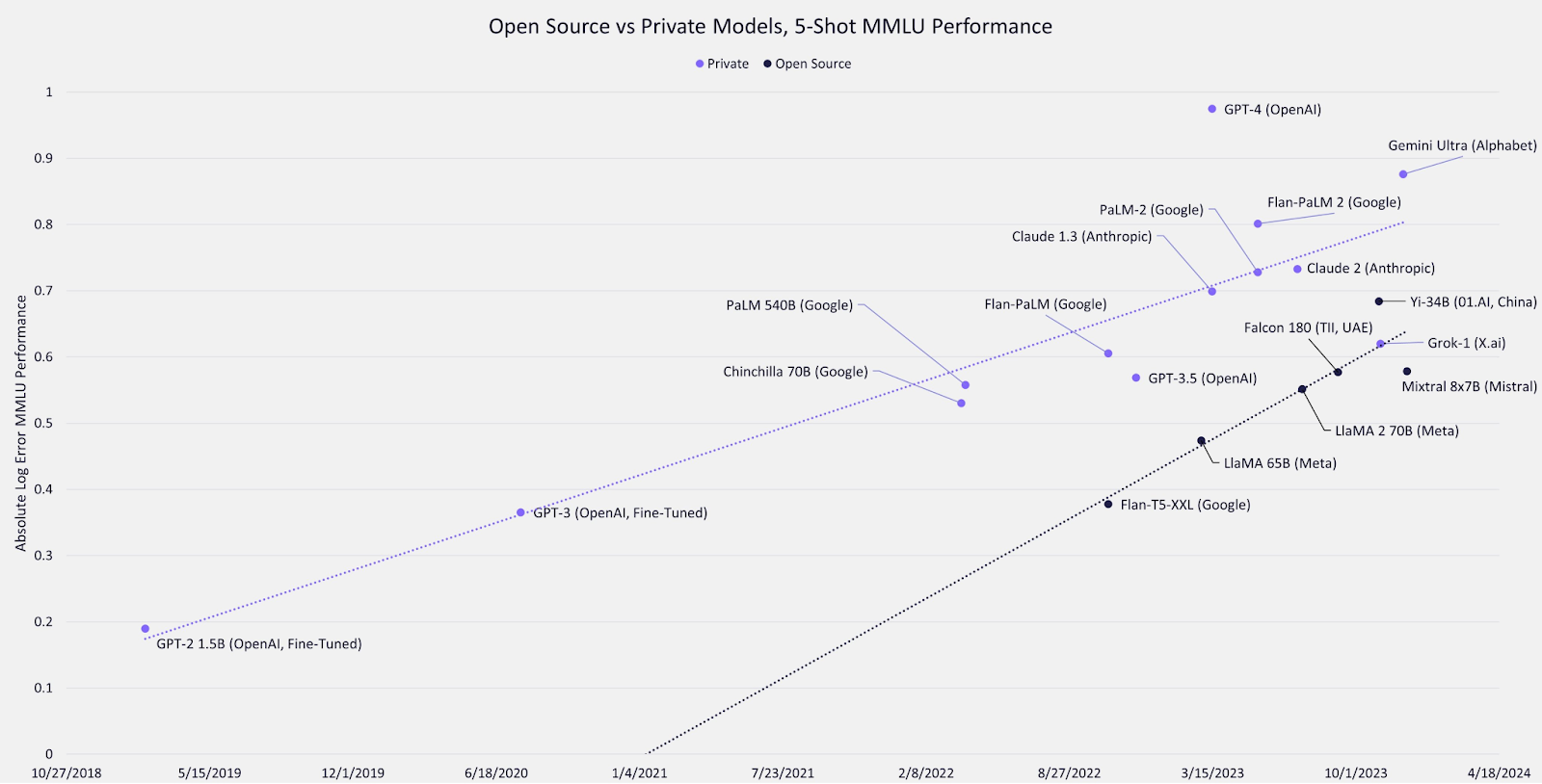

Here’s a recent graph from ARK Invest. Note the trend line angle for open source LLMs performance on the bottom vs. closed source on the top. If those lines intersect by 2026, people will no longer be saying that open source LLMs will always lag proprietary models by 6-12 months.

The money flow into electric vehicle technology continues based on strong customer demand. Don’t be fooled by recent articles about Tesla and Rivian throttling back investments - that indicates short-term over-investment in the West in the current generation of battery tech, but China’s EV growth has been massive, and many startups are racing to build the next generation of electric battery and supporting infrastructure. I expect the sector to go through a series of S-curves.

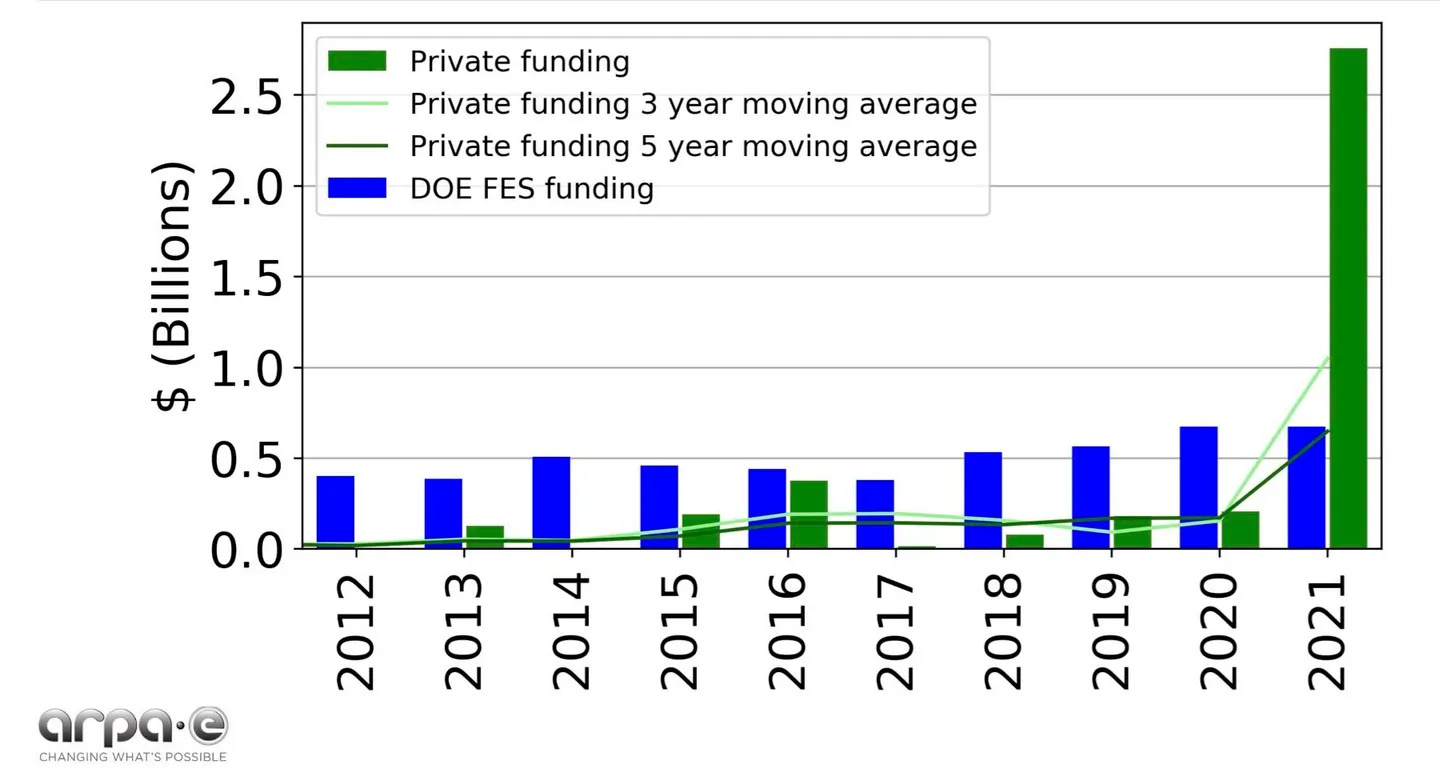

Looking further out, in 2023 we saw critical early milestones in nuclear fusion (e.g. Lawrence Livermore repeated their net positive reaction three times), and space based solar power, suggesting that commercialization estimates for both might get pulled in from the 2040s to the 2030s. This chart below is eyebrow raising - for the first time ever in 2021, private investment in fusion soared beyond public investment. And then it doubled again in 2022 to nearly $5B (source: PowerMag).

Although it may seem counter-intuitive that a sector requiring high capex cost and a long timeline to exit could grow while interest rates are rising, it can be explained by a few factors, such as: (i) a crossover of VC investors from the ESG/climate space, (ii) regulation and legislation providing tailwinds for clean energy (along with continued growth of carbon credit markets), and (iii) “de-globalization” driving more US investors to bet on energy independence.

Defense: This recent NYTimes article about DoD/Pentagon people joining VC firms is a lagging indicator. The number of defense deals I saw on AngelList in 2023 was up by many times any prior year, ranging from from physical attack and defense technologies to cybersecurity and intelligence gathering. Multiple startups attempted comps to Anduril, Palantir, and Shield AI, while advertising “dual use” business models, with near-term government grant funding exceeding commercial revenue (and in some cases, exceeding Series A equity investment amounts). The Anduril and Palantir “mafias” have created an ecosystem friendly to new defense startups, and the willingness of the government to make SBIR and other grants to startups has grown sharply during the COVID years. Crunchbase had a well balanced review in Aug 2023 of the hype around the defense sector.

2023 Exits:

My Asymmetry Ventures portfolio had one exit in 2023: a SPAC for Volato (fractional ownership of private jets), which is trading as $SOAR. Like most SPACs the last few years, it is trading below initial price, but I remain bullish on the business.

Gold Dragon Ventures syndicate had one exit in 2023: WeLoveNoCode (no-code hiring marketplace) acquired by Toptal.

My angel portfolio had a few minor exits:

Notable Labs (personalized precision medicine for cancer) merged with VBL Therapeutics ($VBLT).

Clearbit (website visitor intelligence for CRM) acquired by Hubspot.

Properly (Opendoor for Canada) acquired by Pine Canada.

PriyoshopSeed: The leading B2B e-commerce and logistics provider of packaged goods to corner stores in Bangladesh.Crossed $200M annualized GMV / $10M annualized revenue (5X year-over-year growth), investing alongside Iterative (Mercury, Spenmo), SBK Tech Ventures, BANSEA, and Voltity (Revolut).

Volopay Series A+: Fast growing corporate expense and credit platform for Southeast Asia. Backed by Antler, VentureSouq and JAM Fund.

SFA Therapeutics Seed+: Revolutionary treatments for curing autoimmune disorders. Led by North South Ventures, after strong Phase 1b results in treating psoriasis.

Pirouette Medical Series A+: Reinventing the needle. Led by Safar Partners.

Endiatx Seed: Pill-sized robot endoscopy. Backed by Mayo Clinic Ventures, the American Gastrointestinal Association, and Tale Venture Partners.

Quantum Designed Materials Seed+: Room temperature semiconductors without the LK-99 hype. Backed by Larry Ellison’s fund and various corporate VCs.

EarthGrid Seed: Digging tunnels with robots using plasma torches - Infrastructure 2.0.

Slingshot Aerospace Series A+: The leader in space situational awareness (i.e. avoiding collisions with space debris). This round follows their double acquisition last year of Seradata and Numerica. Backed by Sway Ventures, ATX and Lockheed Martin Ventures.

Quaise Energy Series A+: Deepest geothermal energy provider ever. Backed by Prelude Ventures and Safar Partners.

Cytoreason Series B (in progress): Leader in machine learning disease models with half the top 10 pharma companies as customers. Backed by Pfizer and a Tier 1 UK investment manager.

New deals backed by Asymmetry Ventures and/or the Rob Ness Syndicate:

Fortuna pre-seed: LLMs for generating legal appellate briefs and predicting case outcomes. Backed by Harvard Innovation Labs and HBS Alumni Angels.

1010 Solutions (dba Liquid Trees) pre-seed: Sequestering carbon with algae in rivers. Backed by Unruly Capital, Aleka Capital, Nordwind Capital and Tiny VC.

Shared Studios seed: Wall-sized business communication portals. Backed by JLL Spark.

Ex-Human seed: Chatbots for dating. Founded by lead engineer from Replika. Backed by Soma Ventures, Terra VC and Metavision International.

Epibone Series A: 3D-printing replacement bones from your own cells. Backed by Kendall Capital Partners and Cedars-Senai Accelerator.

Quidnet Energy Series B+: Storing wind/solar energy underground as geomechanical energy. Led by Breakthrough Energy Ventures, with OurCrowd and Grantham Foundation.

Gold Dragon Ventures syndicate follow-ons:

Green Canopy Node seed: Green home builder. Rapid assembly of internal systems (HVAC, plumbing, electrical), backed by YC, Techstars, and Magnetar.

CapConnect+ Seed+: Digitized corporate bond issuance. Backed by Fusion Fund and Hourglass Venture Partners.

Corvus Robotics Seed+: Warehouse inventory management with autonomous drones. Backed by S2G, Spero Ventures, and Stellar Ventures

Gold Dragon Ventures new investments:

Finfra Seed: The leading embedded lender in Indonesia. Backed by Hustle Fund and AngelList Access Fund.

Wispr.ai Seed+: Silent speech via wearable neural interfaces. Backed by NEA and 8VC.

Ordaos bio Seed+: Generative AI platform for mini-protein design. Backed by Middleland Capital and Route 66 Ventures.

Orbillion Bio Series A: The leader in premium lab grown meat from stem cells. Backed by YC, AngelList Access Fund, At One Ventures, Metaplanet, and VentureSouq.

Dimensional Energy Series A: Sustainable Aviation Fuel leader. Backed by United Airlines Ventures and Envisioning Partners.

Emerge Series B: Ultrasonic virtual touch over the Internet. Major deals with Disney and Sony. Backed by Soma Capital, Tamarack Global, Eric Schmidt’s Steel Perlot fund, and family offices from Riot and Blizzard founders.

Flexport secondary: Unicorn digital freight forwarder. Backed by A16Z, Softbank, Founders Fund, DST Global, Google Ventures, Initialized Capital, and FJ Labs.

Co-syndications with other AngelList syndicates:

TRL11 pre-seed with Mana Ventures: Fast video encoding in space enables remote maintenance/ops. Sourced by Gold Dragon Ventures. Backed by Boost VC and Anorak Ventures.

Cambridge Terahertz pre-seed with futureland: MIT spinout providing security from 3D imaging at terahertz frequencies (radar on a chip). Backed by Silicon Catalyst and Good Growth Capital.

Decode Bio Pre-Seed with Reinforced Ventures: Quantum dots for drug discovery (disrupting DNA-encoded libraries).

ROOK Pre-Seed with Allied VC: API for wearables health data. Backed by Hilltop Ventures and Techstars.

Lavo Life Sciences Seed with Jeff Heitzman: AI for drug formulation. Backed by Undeterred Capital and BBQ Capital.

Charter Space Seed with Jolt VC: Program management SaaS for space missions. Backed by MMC and Techstars.

GPUAudio Seed+ with Davidovs VC: Audio processing on GPUs. Backed by RTP Global.

Centivax Seed+ with Ergo Bio: Broad-spectrum vaccines. Spinout from Distributed Bio, backed by NFX and Global Health Investment Corp.

Klasha Seed+ with Sajid: Cross-border payments for African business. I invested as an angel at the seed stage. Backed by Greycroft and AMEX Ventures.

AlumnaPower Series A with Jolt VC: Aluminum-air batteries (higher energy density than lithium batteries) from recycled aluminum. Backed by Starbridge Venture Partners.

Turn Bio Series A with Jolt VC: Making cells younger by reprogramming the epigenome, without making stem cells. Backed by Khosla Ventures and Methuselah Foundation.

Sepion Technologies Series A+ with Calm Ventures: Lithium-metal batteries increase EV range by 40%. Backed by Airbus Ventures and Fidelity’s Fine Structure Ventures.

Gotenna Series 1 (recap) with Chaos Ventures: Leading mobile mesh network for military and first responders. Backed by Founders Fund and Union Square Ventures.

Three secondary offerings with Ventioneers: Databricks, Epic Games, and Coreweave.

Fund update: I putthe Africa fund plan on hold because my potential co-GP was no longer able to move to Kenya. In addition, Africa startup market conditions worsened dramatically in H2 2023 from a mix of currency shocks and shutdowns. However, I think we’re near a bottom in the overall early stage fund market, and I’ve started planning for a fund in 2025 with a focus on long term defensibility in the sectors of biotech, space, energy, chips and other deeply technical markets. There’s a cyclical debate among VCs as to whether “deep tech” sectors are a good fit for the VC funding structure. Leo Polovets has an excellent quantitative analysis on why it’s reasonable to be bullish right now.

Thanks for reading Contrarian Angel! Subscribe for free to receive new posts and support my work.