Portfolio construction

In most every popular startup investing book, blog or podcast, you’ll find the topic of portfolio construction - that is, how is your bankroll best allocated across startup investments? This usually breaks down into two questions:

How many initial investments should you make (and the closely related question of how much you should invest in each)?

What percentage of funds should you reserve for follow-on investments in your winners at later investment stages?

This usually leads to discussion of power laws, because the majority of venture returns come from a very small number of home run investments.

Here are a few examples that lay out the basics with clarity:

https://www.toptal.com/finance/venture-capital-consultants/venture-capital-portfolio-strategy

https://www.ben-evans.com/benedictevans/2016/4/28/winning-and-losing

At the surface level, this should be familiar to the current generation of public equity investors, because it boils down to one word: diversification.

What you will not find, however, is the concept of sector diversification. Why? Because the conventional wisdom on how to pick early stage winners boils down to some mix of: (i) focus on one or two sectors that you are deeply familiar with, and (ii) bet on great founders rather than the market or business idea.

But funds that focus primarily on great founders, even funds that are explicitly “sector agnostic”, usually end up with portfolios dominated by a limited number of sectors. A few reasons:

Some new sectors may become “hot” in the VC community for Series A funding. These sectors attract a lot of top founders. And seed investors need to pick companies that will get Series A funding.

Network effects relating to deal flow - the more founders and investors you meet from a particular sector, and the more you’re recognized as having experience in that sector, the more likely you are to get intros to other startups in the same sector.

As you learn more about a sector, the time cost of diligence on each new opportunity decreases to some extent.

*Side note - “sector” here doesn’t mean business model or geographic region - for example, some funds specialize in marketplace models, or in emerging market regions.

Here’s my contrarian viewpoint going into 2021: balancing seed stage investments across sectors will generate superior returns over the next decade, due to a variety of trends:

The market is shifting towards an oversupply of early stage investors due to macro-economic trends (e.g. the hunt for yield in an era of super low interest rates, the desire for exposure to asset classes less correlated to stock and bond returns, regulatory changes that increased the pool of potential private company investors)

As more successful VC general partners start seed stage microfunds and VC firms deploy scout programs, adverse selection becomes a real problem for the hottest sectors.

There’s an increased amount of information about startups available to the investing community from accelerators and investing platforms like AngelList. In just a few years, I’ve collected thousands of pitch decks and memos with detailed company metrics, and I’m only doing this part time.

Getting a fair price for great prospects in any one sector is harder than it was a decade ago. Private markets are becoming more like public markets, where indexing tends to provide superior returns relative to risk. To be clear, I’m not saying this is the only factor, or even the most important factor, just that it should be a factor when choosing your startup portfolio.

Another benefit to diversifying across sectors is reduction of tail risk. We’ve seen in 2020 how COVID created incredible tailwinds in some sectors while absolutely decimating others. Even without a Black Swan event, new developments in one sector can disrupt other sectors by changing the relevant total addressable market.

This thesis isn’t easy to execute because there’s very little liquidity available so you can’t easily “rebalance” your portfolio as it grows, and there’s no third party index like the S&P 500 to validate a minimum level of quality. There’s also no black and white definitions of sector boundaries, and there are some great companies that one can easily argue are straddling more than one sector. On the other hand, the growth of syndicates make it easier to invest smaller amounts across a larger number of companies.

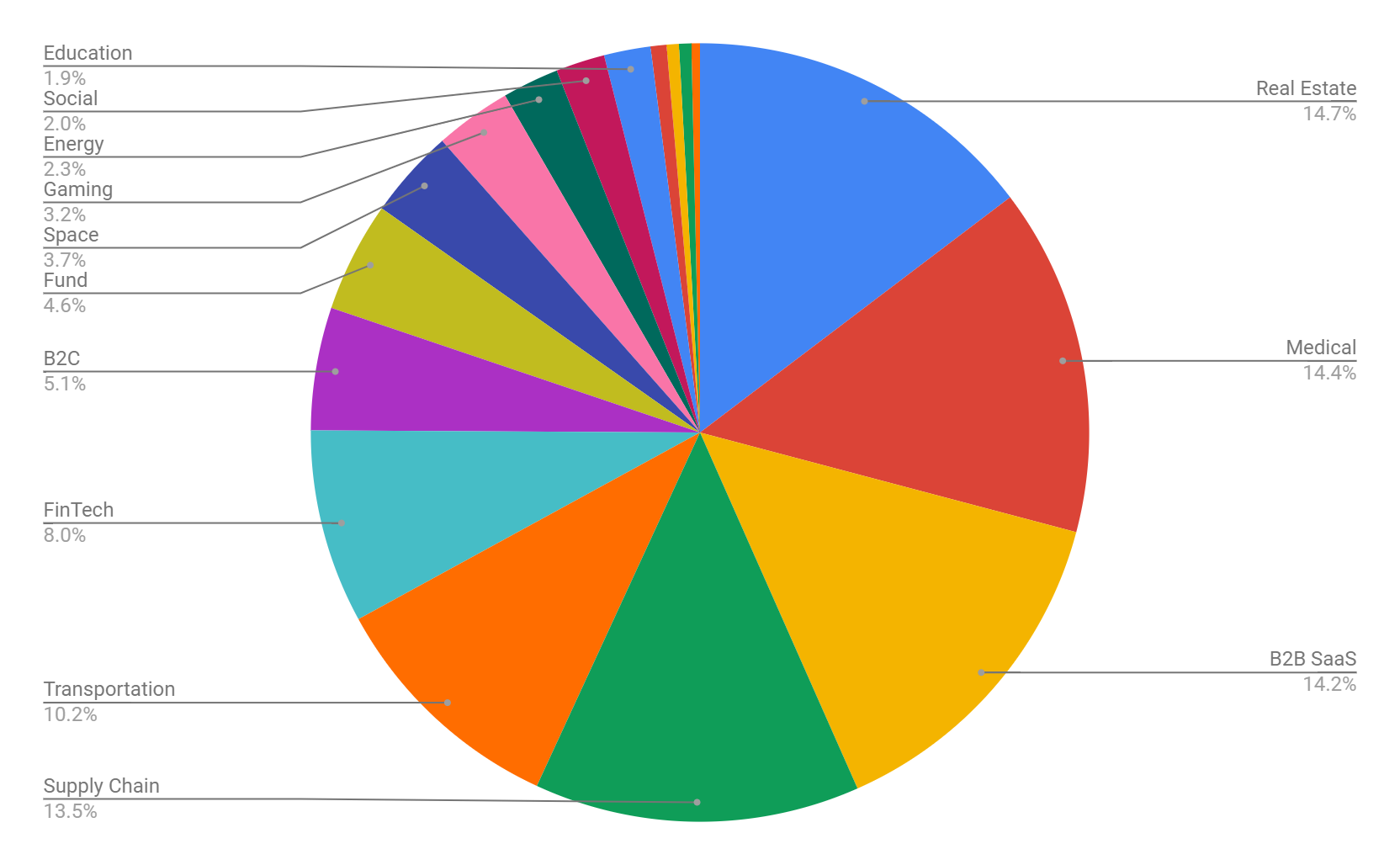

I’ve attempted to balance my capital allocation by sector, but it’s still a bit concentrated in the top 4-5 sectors that I find easiest to assess. The chart below shows data for my first two years of investments.

If you’re an accredited investor, you’re welcome to join my syndicate on AngelList where you can see free deal flow with no obligation to invest.

If you enjoyed this post, I hope you’ll sign up for my weekly newsletter!