Portfolio construction - Part 2

Portfolio construction - Part 2

Bet sizing and follow-on

Today I’m going to cover the two questions I posed at the start of my last post - how much I invest in each company, and how much I reserve for follow-on rounds.

But first, here are a few recent articles in further support of the diversification thesis from last week:

Carta is launching a private stock exchange called CartaX in January.

Fundr launched recently to allow investment in diversified portfolios of private companies.

And now, here’s my contrarian approach on check size: establish a range for seed stage investments that allows sufficient diversification for the bankroll size, but make the range wide (mine is $10K*-$25K), and base the check size for a particular company on the ratio of the expected value** for that company to the current valuation. Strictly investing the same amount in every startup that you want to back is like playing limit poker when you could be playing no-limit poker.

*Some startups will have a minimum investment level above the bottom your range, but don’t invest more than you’re comfortable with, just pass and reassess at the next round.

**I’ll dive into a definition of “expected value” in a later post - for now, I’ll just say that I’m looking for the largest best case outcomes even if the odds of the best case are very small.

One of my favorite books about angel investing is Angel, by Jason Calacanis. I think Jason is a brilliant investor and I’ve learned a lot from him. But Jason recommends investing the same amount in each company at the seed stage for direct investments (i.e. excluding smaller AngelList syndicate investments). And he never directly explains why, although it’s implied that it’s a diversification mechanism:

“After that, in this book we talk about making twenty $25,000 bets and quadrupling down on the winners with a $100,000 follow-on investment. In this model, no one investment is more than 12.5 percent of your angel investing portfolio…”

The most common arguments for standard check size I’ve heard from successful investors on podcasts and blogs are:

Risk of a small portfolio (see Jason above) - If the high end of your range is too high, then you might “put all your eggs in one basket” and not have enough bankroll left to invest in the number of companies needed to find your unicorns.

“KISS” (Keep It Simple Stupid) - There are so many decisions to make as an angel investor, so why not take one decision off the table?

The 500 Startups theory: Nobody really knows which picks will be a home run, so keep it consistent to reduce the chance of a decision error.

Regret minimization: If you write a smaller check for an eventual home run company you’ll be kicking yourself later.

I’ll rebut each of these, and then explain what led me to my position.

Small portfolio: I kept the top of my range not too high, and ensured that my average investment size allowed me to invest in at least my target number of companies. Based on the diversification studies I’d seen, my target was 50, which is actually much higher than Jason’s.

“KISS”: Yes, this makes the job more complex, but I think two of the most critical skills for a startup investor are asset allocation and picking the right founding team. If you’re only comfortable with the latter, you may want to consider focusing on being an advisor or a co-founder yourself.

500 Startups: I want to collect enough info about a startup to have an opinion on the probability of success, not just make a binary decision. And if you aren’t doing this, then how are you deciding if you can accept the valuation? I’m not investing in startups to pick which ones don’t go out of business, I’m investing in startups, and taking the higher risk of loss that brings, in exchange for potentially earning a higher annualized return than I could get from public stocks and bonds. In machine learning terms, I always want to be running a linear regression here, not a logistic regression.

Regret minimization: If I’m finding as much deal flow as I should be, I’ll almost definitely pass entirely on some future unicorns, which feels even worse. Every great investor has. I’ll just have to get over it.

My philosophical argument is that no matter how high my quality bar is for saying yes and investing, there’s always a way to further rank between the startups that qualify. It’s like Olympic gymnastics - every athlete is excellent, but some will get a 9.0 and some will get a 9.7, and the judges will have a mix of qualitative and quantitative inputs to arrive there.

I also look to history on this - some of the greatest angel investing calls ever were very large bets, almost certainly larger than other startup bets those investors made at the time (e.g. Peter Thiel - Facebook, Andy Bechtelsheim - Google, Mike Markkula - Apple).

There’s also a practical reality that led me to this process. I care if the timing of my investment outflows over time is spiky, and I try to smooth it by having a loose quarterly and annual budget, because studying VC returns on startups shows that some time periods are better than others across the board (I assume to macro-economic trends and/or new disruptive technology developments). But the quality of investment opportunities isn’t evenly distributed over time. I’ve had some great clusters of opportunities come in waves, and trying to decide between opportunities forced me to get more precise about ranking them.

Now let’s say my threshold for investing is a 9.0, and I rate Company A as 9.0 and Company B as 9.7. I see some additional benefits to investing a $10-$15K check in Company A beyond diversification: I’ll get information from the company in the form of monthly or quarterly investor updates (make sure you’re getting this!), and if I can get pro rata rights then I might be able to invest more in a later round that otherwise I couldn’t get into at all.

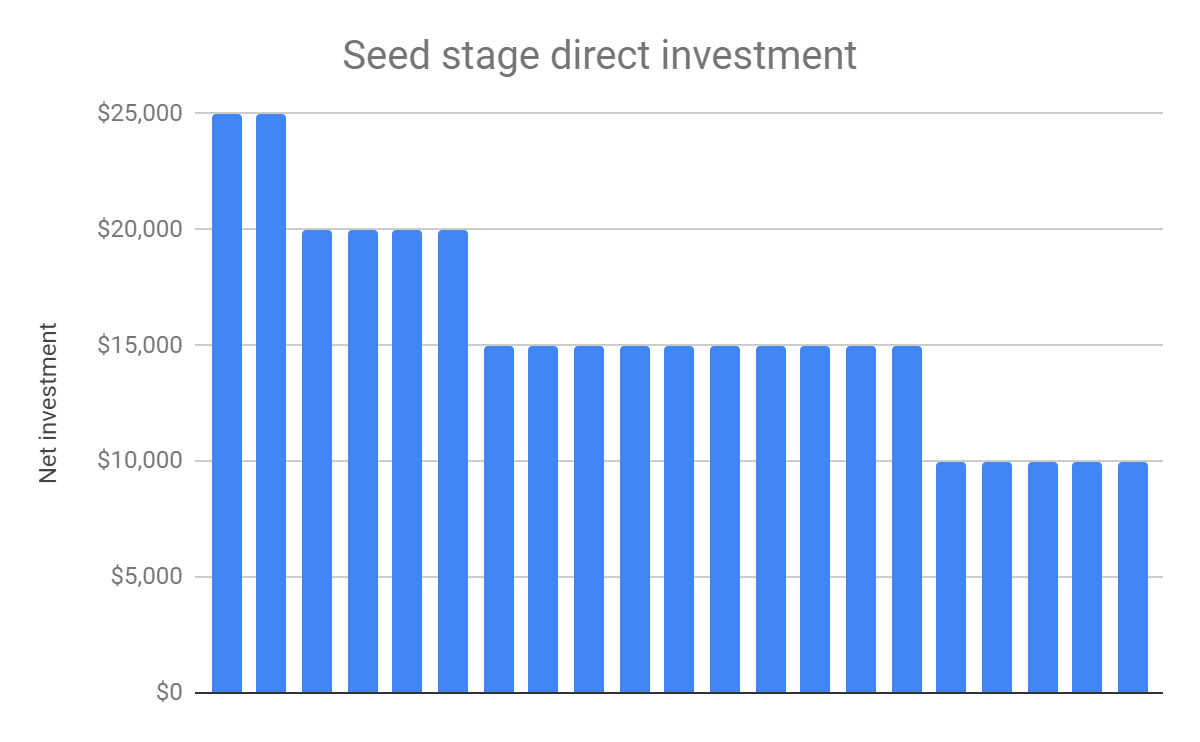

In summary, every angel investor’s returns look like a power law curve, but my initial investment size also looks like a curve (just not as steep a curve). Here’s my first 20 or so:

On the matter of follow-on reserves, I have considerably less conviction that there’s a single right answer. I don’t have enough experience yet. I’ve read advice ranging anywhere from 25% to 50% of bankroll!

I will say this though - while I believe that doubling down on your winners is very important for metrics like TVPI and IRR, as an individual I’m interested in later stage rounds for a completely different reason: cash flow.

Most VCs funds operate on a 7-10 year time scale for a given fund, and don’t expect all returns to be realized any sooner. But they’ll make the initial investments in the first 2-4 years, and then assuming they have some good markups from additional financing rounds in the portfolio, they’ll go out and raise a second fund.

An angel investor invests from their own savings, so that strategy won’t fly. You have to ask yourself whether you’re likely to have other sources of cash flow that allow you to substantially increase your startup investing bankroll over time. I do not, and therefore I not only reserved one third of my bankroll for follow-on rounds in my own portfolio, I also set aside 5% of bankroll to invest in late stage rounds (Series B or later) in other syndicates, despite the 20% carry cost. Why? So that I have better odds of smoothing my returns over that 7-10 year time horizon. I think of it as similar to bond laddering. I’m pretty sure more experienced investors would say this is sub-optimal for my total returns, but it provides me better peace of mind.

Thanks for reading! Next week I’m going to share my due diligence process with founders.

If you’re an accredited investor, you’re welcome to join my syndicate on AngelList where you can see free deal flow with no obligation to invest.

If you enjoyed this post, I hope you’ll sign up for my weekly newsletter!