Thinking fast and slow for VCs

Thinking fast and slow for VCs

What shape is your funnel?

Daniel Kahneman’s book, Thinking Fast and Slow, is one of the more memorable popular psychology books, with deep implications for cognitive science and behavioral economics. Kahneman popularized the idea of “Type One” vs. “Type Two” thinking. Type One thinking is fast, instinctive/intuitive, and emotional, while Type Two thinking is slow, logical, analytical, and involves deliberate attention to details. Kahneman’s book showed how Type One thinking is a powerful tool but also leaves us at the mercy of unconscious biases. For investing, Type One thinking is widely understood to lead to mistakes that could be avoided through more Type Two thinking.

I’ve been reflecting on this as I ponder one of the mysteries of VC fundraising - how do I differentiate myself as a capital allocator, and how much should that differentiation relate to the deal evaluation and selection process, rather than deal access or ability to win the desired deal?

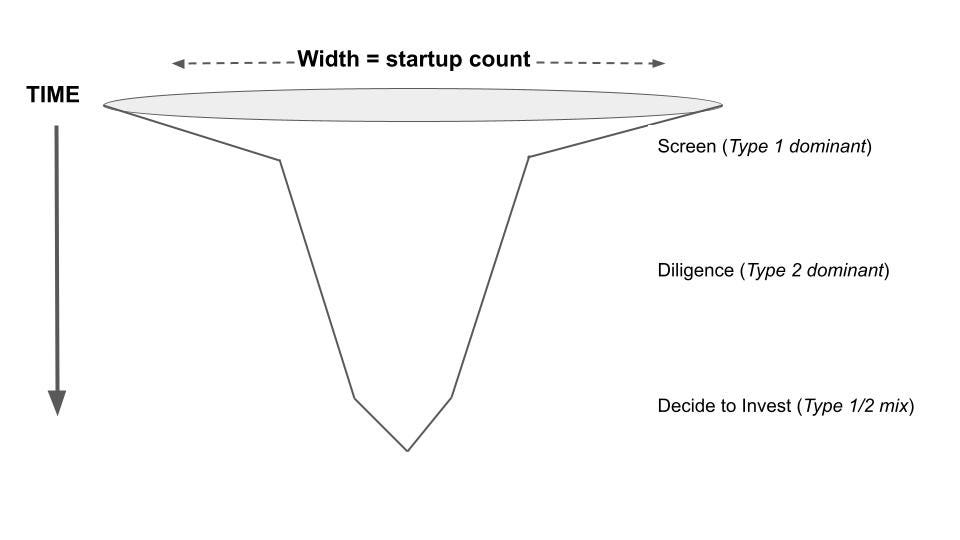

Outlines for VC fundraising pitches usually include slides that (1) show potential to find high quality and quantity of deals in the first place, (2) highlight a funnel process to filter down to desired investments, and (3) explain why founders would want to take the VC’s money for those deals. But they rarely include details about the funnel process other than the number (or percentage) of deals filtered at each stage, perhaps with a slide that looks something like this:

This is only used to show filtering of the number of candidates (X axis) over time (Y axis), and is not actually drawn to scale.

In rare cases there might be information about the time for each stage, such as this:

Now back to Kahneman. For early stage startups that have isolated windows of liquidity, and don’t have quarterly earnings reports, an S-1, or in many cases even audited financials, Type One thinking is absolutely required, quite unlike investment funds that strictly invest in public companies. There’s simply too much unknown information. Successful VC funds will also have a rigorous and repeatable analytical framework for Type Two thinking,

What I’m interested in is how and when VCs mix Type One and Type Two thinking at different points in the deal funnel.

At the top of the funnel everybody has an objective first pass filter - this isn’t really Type One or Type Two, it’s a fast and automatic rule-based elimination of deals that don’t fit the fund thesis promised to the fund’s LPs (e.g. based on business sector, startup stage, or startup location).

Next comes the Type One instinct to decide, after the first meeting or first deck review, which deals deserve continued investment of time. Some VCs maintain a policy with additional KPI thresholds (e.g. level of revenue, growth rate), but in practice there will be exceptions based on other factors.

In the next phase, VCs dig in over subsequent meetings/calls/emails to get more information and verify details. To be fair, I’m collapsing into one stage here what might be considered two distinct processes by bigger funds: (i) info collection that is filling in known unknowns before an investment committee gives a green light to send a term sheet, and (ii) rote fact verification that might come after the term sheet but before the final contract with funding. These steps tend to be almost entirely Type Two thinking, potentially using a fixed checklist of questions or documents required.

Last, there is the final decision phase. The deal partner writes an internal memo reviewed by other partners, and in some cases may include a quantitative “scorecard” with ratings along various dimensions important to the fund, perhaps including a few financial cases (base case, bull case) with probability of outcomes, leading to the output of a score that allows ranking between deals. This phase mixes Type One and Type Two thinking, and while most VCs would honestly assert it is more of the latter, I believe in practice most firms lean heavily on Type One thinking at this step, especially for earlier stage companies, when it comes to scorecard inputs such as probability of various exit outcomes, comps, and limited financial data exit comps).

Here’s the shape of the funnel I’ve described if we were more accurately plotting the time dimension, based on the angle of the sides:

What I do differently is that I aspire to reverse the mix of Type One and Two thinking at each stage of the funnel, which I believe leads to more information and better outcomes. The shape of my funnel is more like this:

I’m aiming to use more Type Two thinking up front, more Type One thinking in the middle, and more Type Two thinking again at the very end. If the average VC is using 75% T1 at the top, 10% T1 in the middle, and 50% T1 at the end, I’m shooting for 50% T1 —> 75% T1 —> 25% T1. Put another way, I reduce the information error bars and improve the quality of analysis with more Type One thinking earlier in the process and more Type Two thinking later.

I’ll wrap up with a few reasons why I believe this matters:

At the top of the funnel I have to cast a wide net, but also don’t want to miss critical objective information. Even if I pass on the deal at hand, that information might also have value for other deal evaluations, so it’s worth a little extra time investment.

In the middle, speed is very important - all but the most famous VCs risk adverse selection for the highest quality deals if they can’t move fast enough during the diligence phase. However, I don’t believe in using fixed checklists of questions after the first meeting to obtain that speed. I start from a sector dependent outline, but many questions I ask are based on the prior answer rather than on a preset list. I often improvise a line of questioning that elicits information I wouldn’t otherwise obtain. This is the path to find unknown unknowns, which is harder to do with a Type Two process here. In short, the most valuable intel that isn’t in the pitch deck comes from a conversation rather than an interview.

At the end, when I’m deciding whether to invest and how to rank the deal among all the deals in the pipeline, I once again revert to more deliberate analysis. The painful mistake after narrowing to a handful of good deals is moving forward on the A- rather than the A+ deals, because VC returns are driven by power laws. The final decision cannot be based solely on a gut feeling that the founder is a genius, the technology is world changing, or things of that nature, even though that is often a part of the picture.

Curious to hear your thoughts if you have a different point of view - let me know!

Maybe we all have different little metrics. I have one which I'm not sure if it fits in type 1 or type 2. I screen for the company having real customers with a bit of up and to the right trend, even if a tiny base. That has served me well, especially for b2c