Time Horizon

Hi all, this week I’m going to be talking about liquidity and time horizons. A common friction point for new startup investors is the uncertainty around when they will get their money back.

Most closed VC funds set expectations of a 7-10 year time horizon for the fund to see significant returns. For individual investments, that may be the average, and may even have the median embedded within it, but the tails on this distribution are very wide. You might have a seed stage company that’s purchased within 18 months after you invest, while another might take 15 years to go public. Is there a way to better predict this? Does this uncertainty make the asset class less attractive?

First, let’s take a look at some metrics.

Crunchbase published some data here that shows median times to IPO, with companies grouped by sector: https://about.crunchbase.com/blog/startup-exit/

McKinsey showing that, over the last 30 years, companies are staying private for much longer on average (but note, this does not mean they are growing more slowly, in many cases, the time to hit a $1B or $10B private valuation has decreased): https://www.mckinsey.com/industries/technology-media-and-telecommunications/our-insights/grow-fast-or-die-slow-why-unicorns-are-staying-private#

While you may want to assume that a startup at a particular stage in a particular sector is likely to IPO within X years because comparable companies are going public today at that age, IPO markets can “open” and “close” based on complex macro-economic factors that have little to do with a particular startup’s prospects. Similarly, if there’s a wave of M&A today, people might speculate that the startup will be bought within X years if it hits it’s milestones. But the appetite for M&A is often based on other non-correlated aspects of large-cap strategy, game theory and macro-trends.

If you will definitely need the money back in the next decade, startup equity probably isn’t the right asset class for you. So your age and current live goals will come in to play. And beyond that, there’s the question of how illiquidity affects perception of value.

I’ll address this in a roundabout way, by discussing the common advice to not invest more than 10-15% of your net worth in private startups. I’ve heard at least three motivations for this advice:

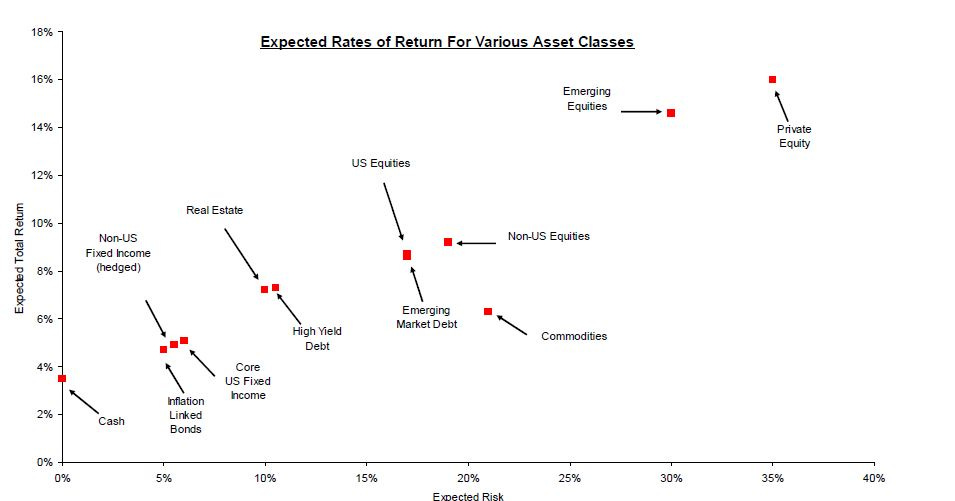

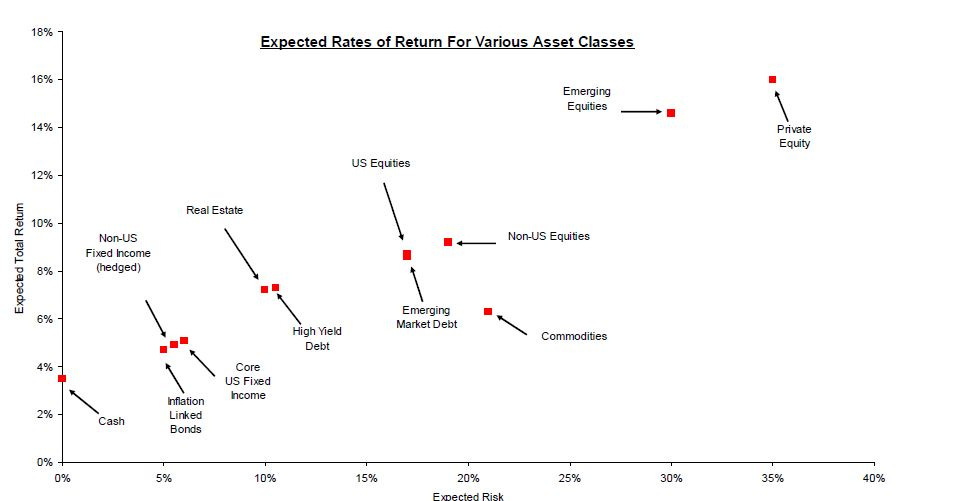

The high degree of risk (returns variance). As most money managers will tell you, portfolio theory suggests a blended asset allocation that meets your personal needs of balancing returns and risks. The vast majority of people have some blend of bonds and equities in their retirement funds as a result. Here’s a chart from the classic2009 Bridgewater paper on “all weather” portfolio construction:

There’s our friend “private equity” (which includes startups) in the upper right.

Startup investing is for sophisticated investors such as VCs. The idea here appears to be that you’re more likely to make unforced errors than if you stick to public equities and bonds. The SEC’s accredited investor limitations play into this, although they started to loosen a few years ago with the crowdfunding JOBS Act.

Lack of liquidity. Once you invest in a startup, there’s no public market where you can sell your shares and get your money back. Although there are some private marketplaces for later stage startups (Forge, Equityzen), the transaction costs are high, there’s no guarantee you can fill the volume you want at a reasonable price relative to the last private valuation, and you’re generally restricted from disclosing detailed info about the startup to the buyer.

While I agree with the first point here, I think the second and third are worth debating. I’ve met plenty of professional finance people with experience in bond trading, M&A, and even IPOs from investment banking, who don’t seem to have any special skill in startup investing. Many of the most successful angel investors historically did not have MBA Wall Street backgrounds.

And I believe that some degree of illiquidity is not always a bad thing, and shouldn’t disqualify startup investing for the retail investor.

The biggest single investment that most people will make in their lifetime is buying a house. Most mortgages are structured such that if you were to sell within the first few years, you would lose money. And selling a house has tremendous personal and financial friction associated with it. I think of the housing market as “partially illiquid” at the individual level, yet most people believe investing in real estate is a good investment.

Warren Buffett, Jack Bogle and many other legends have demonstrated that buying and holding great companies (whether individual stocks or an index fund) is one of the best strategies for maximizing equity returns over a lifetime. But many people (myself included) who buy an individual stock have trouble resisting the urge to sell some if the stock goes up over a relatively short period at a rate that greatly exceeds the overall market. Technical analysts and behavioral economists understand this well. Many people this generation have made good money holding the tech giants such as Apple, Amazon and Google…but how many have held and never sold for decades? Illiquidity can be a feature rather than a bug.

Where points #2 and #3 above intertwine is that the learning loop for startup investing is very slow. It’s difficult to identify problems and improve performance because it takes a long time to get feedback on your past decisions. Therefore, I believe the X% of net worth recommended limit for startup investing should start small and go up gradually over time based on the investor’s personal experience with it.